Summary

- AxoGen has upcoming clinical trial inflection points that must be considered in addition to sales momentum in the back end of this year.

- Cost-targeting & liquidity preservation measures taken by management this year have been realised at the level of operating efficiency.

- The company has reduced the cash conversion cycle, and less cash is tied up in working capital, enabling greater efforts to drive growth to the top.

- We feel shares are worth ~$20, whilst trading at 7.35x EV/gross profit and 5.3x 2021 sales makes the valuation attractive also.

- Here we cover the necessary updates to the moving parts in the investment debate, for the benefit of one's own investment reasoning.

Investment Summary

We are bullish on AxoGen (NASDAQ:AXGN) shares, and are confident on upcoming inflection points coupled with Q3 performance, to advocate for entry in the coming periods. AXGN's peripheral nerve repair/graft segment has held up well against the current standard of care regimen, standing up against competitors on efficacy. AXGN also has key exposures to expanding addressable markets in neuropathic pain, breast sensation following mastectomy, oromaxillofacial ("OMF") nerve interventions, carpal tunnel repair and many others via their porcine submucosa extracellular matrix ("PSECM") route. Given these exposures and the implied growth prospects in each market, we feel that AXGN has potential to capture additional market share as revenue drivers continue to begin to build speed over the coming periods.

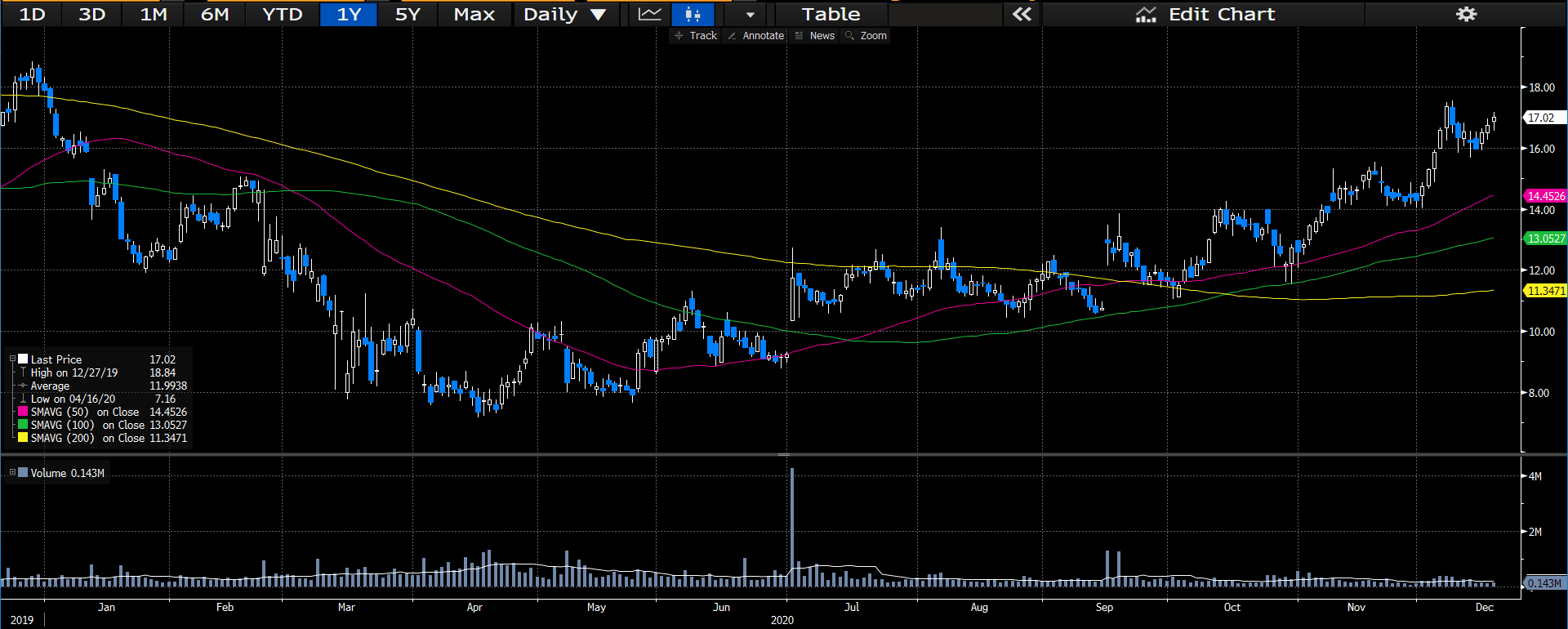

Figure 1. Single-year price. performance

Data Source: Author's Bloomberg Terminal

Balancing these levers to growth is the current economic environment and capital-intensive operating mix, in addition to the carry through of stressors faced by the company this year. We feel these weigh into the investment debate and bring the equation back towards a more symmetrical risk/reward profile. Here, we provide the necessary updates to the moving parts within the investment debate, and weight all of the factors for consideration to assist investors in their own investment reasoning.

Q3 Walkthrough Supports Narrative In Operating Efficiency and Addressable Market Growth

Q3 financials came in well above consensus and provided evidence of a good runway for growth into the coming periods. The top-line came in strong at ~$33 million, exhibiting ~17% upside YoY. Much of the sequential growth pattern in Q3 was defined by a pull-through of procedure deferrals, which had benefitted from a recovery in volumes, and contributed ~10% of total sales for the quarter. Organic growth therefore is contained to ~6% YoY, still impressive considering the inpatient environment YTD and impact of the pandemic on the wider medical devices/appliances end-markets, including implied incidence of trauma cases at the back of this. The company has also engaged in sound cost-targeting and liquidity preservation measures this year, which have been reflected in lower sales rep headcount, and at the productivity plus operating efficiency levels.

To illustrate, accounts receivable turnover remained relatively flat YoY, whilst days of sales outstanding increased ~9% to 58 days, meaningfully lower than peers across the YTD. Impressively, inventory turnover actually increased ~25% to 1.64x, whilst the days of inventory outstanding reduced by 50 days YoY to 223 days, again well ahead of competitors this year amidst the current pandemic-induced environment. The company also managed to increase accounts payable turnover by ~20% to 5.28x, reducing the accounts payable turnover days by 13 days to ~69 days. This shows the company's ability to settle transactions and increase the depth of working capital efficiency, being able to pay the bills as it were, to add torque working capital cycle. As such, the cash conversion cycle reduced by ~47 days YoY to 211 days, which carried through to a 50 day reduction to 281 days. Therefore, targeting efficiency measures engaged by management this year have carried through the cash flow statement and into operating efficiencies, and the company has managed to reduce the amount of cash tied up in working capital and increase the conversion rate of inventory to cash. Therefore, we feel the company is well-positioned to continue this trajectory and capture additional market share from competitors, who are lagging in productivity on the back of challenges faced from the pandemic this year.