Summary

- Share price has moved outside of historical norms relative to competitors.

- Company utilizes more aggressive accounting methods than others.

- Expect 30%+ retrenchment in share price relative to others.

COVID has thrown the entire world for a loop with non-essential industries such as tourism obviously taking a much larger hit than other sectors. When or if operations and pattern of historic profitability will return is impossible to know but in periods of great uncertainty and fast moving markets mis-pricing occurs and that appears to be the case at this time with Royal Caribbean Cruise Lines (RCL) becoming over-valued relative to both Carnival Corporation (NYSE:CUK) and Norwegian Cruise Lines (NCLH).

This article will be organized as follows:

- Background on historic profitability and relative size of major cruise operators.

- Discussion of Accounting Methods.

- Relative Valuation Estimates.

- Conclusion.

Some issues that were not explored in-depth that constitute risks to the above assessment are:

- Things are moving fast with numerous debt and capital raises taking place and more to come in the future. In such an environment, the ability of management to negotiate such agreements with investors as well as blind-luck can have a long-term impact of shareholder value. RCL might very well be superior in this regard but it was not obviously the case.

- All companies face the risk of margins collapsing on a medium-term basis and it is not clear that any will survive without bankruptcy reorganization but there are reasons for hope.

- Analysis which follows will utilize the share price of Carnival plc (CUK) rather than Carnival Corporation (CCL) in making market capitalization calculations as they have the same economic interests. The fact that the price of these two securities have recently diverged in a significant fashion is further indication that markets are not cold calculators of economic value and that opportunities may exist despite the great stress these companies are currently under.

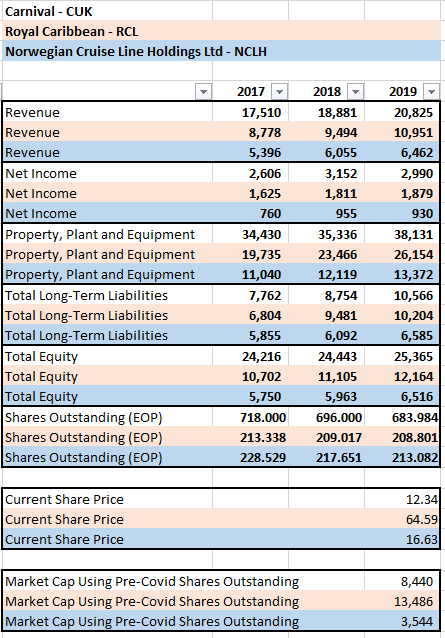

Historic Operations

Data Source: Guru Focus

Simply eye-balling the above would lead to the following questions:

- Why would the market capitalization of RCL exceed that of CUK given that the latter is a significantly larger and a more profitable operation with less debt? This is a deviation from historical patterns.

- Why wouldn’t NCLH have the same relative market capitalization given that its pre-COVID operations and balance sheet (adjusted for smaller operational base) are so similar to RCL?

No adequate answers to the above could be located and as a result, it appears RCL is overvalued relative to both CUK and NCLH.