Summary

- FNF's valuation both absolute and relative to the S&P 500 has reached historic lows and is unjustified.

- Fundamentals (both internal and relevant macroeconomic) are as strong as ever evidenced by record 2Q20 revenue, operating margins, and EPS.

- Multiple catalysts to correct the valuation dislocation exist in the next 3-6 months, including potential inclusion in the S&P 500 Index.

- Track record of incubating and spinning off technology businesses (FIS and BKI were both spun out of FNF) provides added upside potential.

- Believe shares offer 60-100% upside immediately using standard valuation analysis.

Company Overview

Fidelity National Financial (NYSE:FNF) is the nation's largest and most profitable Title Insurance & Settlement company with nearly a 34% market share. FNF's "recent" history began in 1984 when Bill Foley and a group of investors bought out what was then a small title company in Arizona with ~$40mm of revenue. Over the following years, 80+ roll-up acquisitions and a relentless focus on operational efficiency have led to its current market-leading position.

The key to FNF's success has been two-fold: its above-mentioned focus on operational efficiency, and leadership in technology.

FNF's revenues come from processing both residential and real estate transactions and refinancings. The volumes are highly correlated to transactions completed in both segments, and price per transaction generally is a % of sale price. Revenues are highly dependent on the health of the real estate market in the United States.

Although the different real estate volumes and refinancings can fluctuate greatly, FNF's results have been steady. This is the result of the variable cost structure and aggressive expense management systems. When volumes slow down, it quickly reduces headcount and does more with less. As you can see over the past 10 years, the company has grown EPS at over a 19% CAGR and limited volatility:

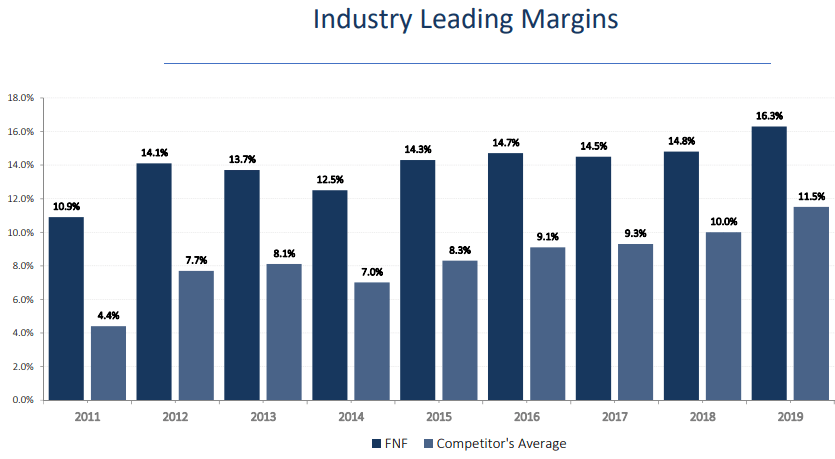

While all title companies manage their expenses in relation to volumes, FNF has been the best operator in the group. Its title agents are generally the most productive, and it gives the regional managers the proper incentives and autonomy to react to changing market conditions by changing headcounts at the local level in real time. This combined with scale advantages has led to consistent outperformance of title operating margins vs. competitors.

Technology is also an advantage. FNF has consistently bought and developed ancillary technology businesses that both enhance its efficiency internally and offer other services beyond the title market. It may come as a surprise to learn that that both Fidelity National Information Services (NYSE:FIS) and Black Knight, Inc. (NYSE:BKI) were once wholly owned by FNF and spun out. Although those companies are no longer under the FNF umbrella, others are being grown in their early stages. Management's track record of adopting and growing technology products within FNF is impressive.

Technology is also an advantage. FNF has consistently bought and developed ancillary technology businesses that both enhance its efficiency internally and offer other services beyond the title market. It may come as a surprise to learn that that both Fidelity National Information Services (NYSE:FIS) and Black Knight, Inc. (NYSE:BKI) were once wholly owned by FNF and spun out. Although those companies are no longer under the FNF umbrella, others are being grown in their early stages. Management's track record of adopting and growing technology products within FNF is impressive.