Summary

- Fidelity National Financial is a leading provider of title insurance and transaction services to the real estate and mortgage industries.

- The housing market has shown strong resiliency during the current recession.

- The F&G acquisition adds both diversification and earnings accretion.

Fidelity National Financial (FNF) has seen its performance lag that of the broader market by a fairly wide margin on a year-to-date basis. Since the start of the year, FNF has returned a negative 27%, compared to the 4.4% return of the S&P 500, which currently sits just a hair below its all-time high. Evidently, FNF has been left behind by the market rally over the past four months, while an enormous transfer of wealth has flooded into the tech sector, which has been a net winner this year. In this article, I evaluate why I believe FNF’s underperformance is unwarranted, and what makes this an attractive long-term investment; so let’s get started.

(Source: Fortune)

A Look Into Fidelity National Financial

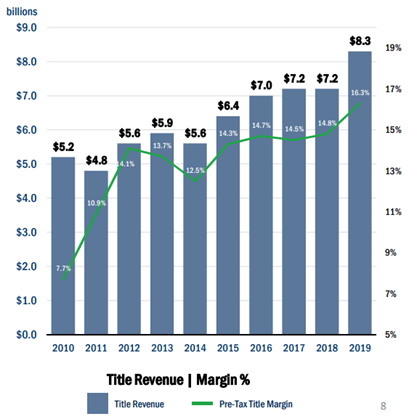

Fidelity National Financial is a leading provider of title insurance and transaction services to the real estate and mortgage industries. Its title insurance business is the largest in the United States, and operates under the names Fidelity National Title, Chicago Title, and as three other regional title insurance underwriting companies. As seen below, FNF has had a strong track record of steady revenue growth over the past decade, growing at an annual CAGR of 5.3%, from $5.2B in 2010 to $8.3B in 2019.

(Source: Company Investor Presentation)

What’s more impressive is that through investments in technology and operating efficiencies, FNF has also steadily improved its margins to 16.3% in the latest fiscal year. This has helped the company grow its operating income at a faster rate than revenue. This is demonstrated by FNF’s operating income growth, from $607M in 2010 to $1.47B in 2019, representing an impressive 10.4% CAGR over this time frame.

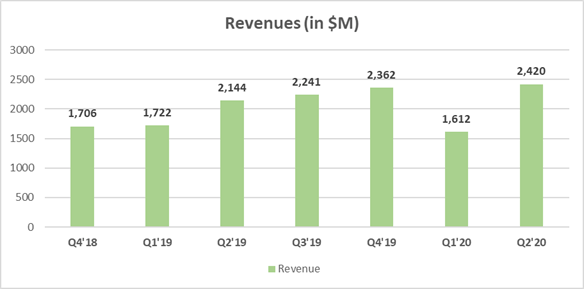

More recently, COVID-19 has been a key risk factor, as it resulted in a 6% drop in revenues back in Q1’20. However, as seen below, revenue quickly bounced back during Q2, with $2.4B in sales, representing an impressive 13% YoY growth.

(Source: Created by author based on company financials)

This YoY increase in revenue was helped by a wave of refinance activities due to low interest rates, which, according to management, were up 111% compared to the prior-year quarter. One risk factor that investors should be mindful of, however, is the recent announcement by Fannie Mae (OTC:FDDXD) and Freddie Mac (OTCQB:FMCC) that, starting in September, a 0.5% fee will be applied to mortgage refinances. While it remains early to be seen whether lenders will absorb this cost or pass it onto borrowers, it is something that could put a damper on future refinancing activity.